NEA’s water poverty lead Jess Cook reflects on the challenges facing those struggling with debts, and encourages them to take #TheFirstStep

This week is Debt Awareness Week[1] – a week to raise awareness of free and impartial debt advice, encouraging those in debt to take #TheFirstStep in their journey to becoming debt free.

It also marks one year since the first lockdown was announced in the UK; a year of lockdowns and economic uncertainty which has resulted in a substantial number of people falling into arrears; some for the first time, some falling even deeper into debt.

We know that debt is extremely common with the households we work with. These debts may be held with the suppliers of essential services, or with credit cards, overdrafts, and loans. We also know that many people have debts with friends and family, or, more worryingly, even with high-interest lenders or loan sharks.

Personal debt can be crippling, and it can have a substantial impact on all aspects of life.

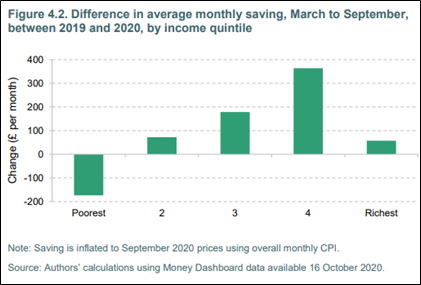

And despite reports of overall debt levels reducing, this graph from the Institute for Fiscal Studies clearly shows how the poorest in our society have been the most affected. Where others made savings on eating out, socialising, holidays, and other luxuries, lower-income households didn’t have those luxuries to cut back on, and many of them are now worse off than they were a year ago.

Source: Institute for fiscal studies, Spending and saving during the COVID-19 crisis[2], October 2020

I hear many people talking about the ‘cliff edge’; wondering when we’ll see the mass influx of financial issues rather than the trickle they might be seeing now. The end-date for furlough approaches, companies ‘get ready’, but at the last-minute support is extended, shifting the goalposts again and potentially masking the problem for another few months.

Furlough is currently available until the end of September. The Universal Credit uplift is due to end then too. By September, based on the current roadmap out of lockdown, we could be back to a relative normality – but could our new normal mean that some jobs and even industries still aren’t viable? If so, that cliff edge is closer than we think.

Our delivery teams at NEA have been working hard to support people with their energy issues during the pandemic. During this time, they’ve helped over 240 people access almost £150,000 of debt write-off, some of whom didn’t even realise they had a debt or hadn’t been aware of (or even chose to try and ignore) how big their debt was.

I was told of a case study where a water company agreed to write-off debts of around £1,000, which suddenly meant the customer could breathe a little easier, sleep a little better, and felt like everything else was more manageable. Imagine how big that debt must seem if your disposable income is only £50 a month, or even less.

I’ve been asked to talk about debt at various events since we published our paper ‘Surviving the Wilderness’ in November[3], to give the people who are struggling a voice. I feel sadness knowing how much this issue has grown, and how many people are now in desperate situations, yet I find some comfort in knowing that this growing issue is at the forefront of many minds, who are all trying to find the best solutions for their customers.

But is it enough that some organisations are looking at what they can do individually?

We have been calling for sectors to work together to identify affordability issues and recommend that a financial vulnerability flag is developed and shared via the Priority Services Register, to give organisations the opportunity to provide support as early as possible. We also want to see the powers of the Digital Economy Act maximised, to ensure people are targeted effectively.

Ofgem’s announcement of the price cap increasing to cover the costs of increased bad debt in energy has been greeted by a lot of negativity. Raising bills to cover bad debt, which has built up because people can’t afford to pay, just results in them paying more. With the legal constraints behind the price cap, this may have been the best option available, but are other industries all going to do the same?

The health crisis has resulted in a debt crisis, and NEA feel that UK Government have a role to help reduce personal debt levels accrued during the pandemic, to stop pushing those who are only just about managing into financial difficulty. Our calls to make the Universal Credit uplift permanent and for Government to reinvigorate Fuel and Water Direct[4], including a payment matching mechanism for debt clearance, are two examples of how this could be achieved. Initiatives like this could be considered in the development of a wider debt strategy, which we would urge Government to consider as they plan the Covid-19 recovery.

As I write this, we’re less than two months[5] away from the breathing space legislation coming into play, and I’m pleased that we haven’t seen the cliff edge of debt issues before that is in place. That support will be vital to people in debt, it will really give them the chance to freeze everything and take the time they need to get help and agree a route forward. But they don’t need to wait.

There are many charities and organisations offering free and impartial debt advice now. Why wait until another few months of interest and missed payments have accrued? If you’re in debt, or you know or work with someone who is, now is the time to take #TheFirstStep. As restrictions ease, wouldn’t it be a relief to have your financial worries ease too?

[1] StepChange launched their annual week of awareness in 2014. This year it runs from 22nd-28th March – https://www.stepchange.org/partner-with-us/supporting-debt-awareness-week.aspx

[2] https://ifs.org.uk/uploads/BN308-Spending-and-saving-during-the-COVID-19-crisis-evidence-from-bank-account-data_2.pdf

[3] ‘Surviving the Wilderness: The landscape of personal debt in the UK’ – https://www.nea.org.uk/wp-content/uploads/2020/10/Surviving-the-wilderness-final-version.pdf

[4] Outlined in our March 2021 budget submission, available here – https://www.nea.org.uk/wp-content/uploads/2021/02/NEA-Budget-submission-2021_FINAL.pdf

[5] Breathing Space (known as the Debt Respite Scheme) comes into force on 4th May 2021 – https://www.gov.uk/government/publications/debt-respite-scheme-breathing-space-guidance